On March 1, 2015, Eckert and Kelley formed a partnership. Eckert contributed $95,000 cash and Kelley contributed land valued at $76,000 and a building valued at $106,000. The partnership also assumed responsibility for Kelley’s $85,000 long-term note payable associated with the land and building. The partners agreed to share income as follows: Eckert is to receive an annual salary allowance of $30,500, both are to receive an annual interest allowance of 11% of their beginning-year capital investment, and any remaining income or loss is to be shared equally. On October 20, 2015, Eckert withdrew $29,000 cash and Kelley withdrew $22,000 cash. After the adjusting and closing entries are made to the revenue and expense accounts at December 31, 2015, the Income Summary account had a credit balance of $86,000.

|

| 1a&b. | Prepare journal entries to record the partners' initial investments and their subsequent cash withdrawals. |

|

|

| 1c. |

Determine the partners' shares of income, and then prepare journal entries to close Income Summary and the partners' Withdrawals accounts. (Enter all values as positive amounts.)

|

| |

| 2. |

Determine the balances of the partners' capital accounts as of December 31, 2015.

|

|

|

Explanation:

2.

| Interest allowances: |

| Eckert (11% on $95,000) = $10,450 |

Kelley (11% on $97,000) = $10,670

Kramer and Knox began a partnership by investing $59,000 and $51,000, respectively. The partners agreed to share net income and loss by granting annual salary allowances of $56,500 to Kramer and $46,500 to Knox, 12% interest allowances on their investments, and any remaining balance shared equally.

|

| 1. |

Determine the partners’ shares of Kramer and Knox given a first-year net income of $93,800. (Enter all allowances as positive values. Enter losses as negative values.)

|

|

|

| 2. |

Determine the partners’ shares of Kramer and Knox given a first-year net loss of $14,800. (Enter all allowances as positive values. Enter losses as negative values.)

|

|

|

rev: 09_16_2011

Explanation:

1.

Kramer: Interest allowances = ($59,000 × 12%) = $7,080

|

Knox: Interest allowances = ($51,000 × 12%) = $6,120

|

| Balance allocated equally = ($93,800 – $116,200) / 2 = $(11,200) |

2.

Kramer: Interest allowances = ($59,000 × 12%) = $7,080

|

Knox: Interest allowances = ($51,000 × 12%) = $6,120

|

Balance allocated equally = [$(14,800) – $116,200] / 2 = $(65,500)

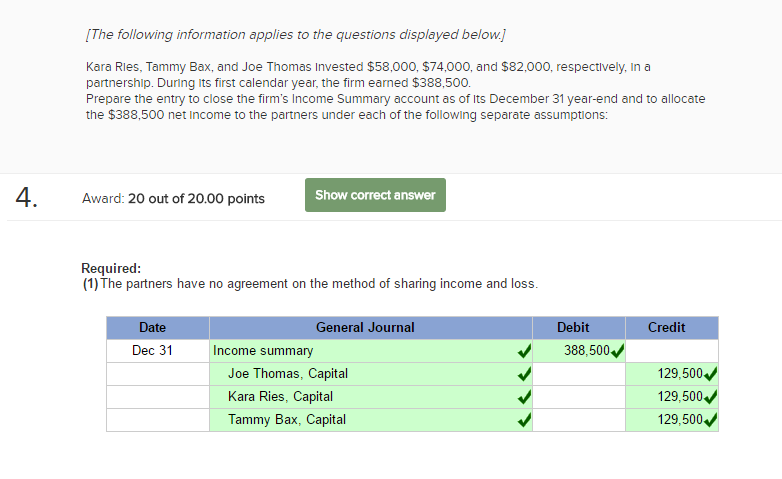

[The following information applies to the questions displayed below.]

Kara Ries, Tammy Bax, and Joe Thomas invested $58,000, $74,000, and $82,000, respectively, in a partnership. During its first calendar year, the firm earned $388,500.

|

Prepare the entry to close the firm’s Income Summary account as of its December 31 year-end and to allocate the $388,500 net income to the partners under each of the following separate assumptions:

|

| Required: |

| (1) |

The partners have no agreement on the method of sharing income and loss.

| (2) |

The partners agreed to share income and loss in the ratio of their beginning capital investments. (Do not round intermediate calculations. Round final answers to the nearest whole dollar.)

| (3) |

The partners agreed to share income and loss by providing annual salary allowances of $35,000 to Ries, $30,000 to Bax, and $42,000 to Thomas; granting 10% interest on the partners’ beginning capital investments; and sharing the remainder equally.

|

|

|

|

|

|